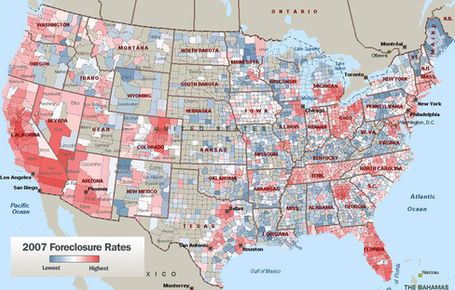

The American Bubble

Beginning in 1999, many immigrants were migrating to the east coast because of cheap homes and available acres, or in other words, “The American Dream”. With new businesses, came new employees, and, therefore, people who needed homes. Demand increased as supply decreased, and prices were inflated. The government in 2001 introduced loan processes that would allow more Americans to own houses. They allowed banks to package mortgages and sell them as an investment to the public. The banking industry grew as did the economy because of more immigrants, more people buying houses, more jobs created, and more spending on needless things.

Investors used two strategies, the first, "sub-prime loans", which were mortgages wrongly given to consumers who wanted houses but should not been granted the loans because the people had bad credit, low income, no reserved funds, and no down-payment (an initial payment provided when the house was bought). The second plan was predatory lending, in which a lender chooses to exploit borrowers by offering them loans they know the buyers cannot afford. These predators simply want to make money in any manner and if these loans were to be defaulted, the loan is usually backed by some sort of collateral--for example, a car or house.

Investors used two strategies, the first, "sub-prime loans", which were mortgages wrongly given to consumers who wanted houses but should not been granted the loans because the people had bad credit, low income, no reserved funds, and no down-payment (an initial payment provided when the house was bought). The second plan was predatory lending, in which a lender chooses to exploit borrowers by offering them loans they know the buyers cannot afford. These predators simply want to make money in any manner and if these loans were to be defaulted, the loan is usually backed by some sort of collateral--for example, a car or house.

|

After a stretch of two years, amateur investors and lenders joined the housing market. The smart investors, understanding the situation, left the real-estate sector, and all that was left were investors that couldn’t afford their ventures and payment through rent could not be trusted. New home costs balanced, used houses weren’t valued as high, and foreclosure of rental properties increased. The next problem, spenders couldn’t refinance as values of prices dropped, minimizing payments.

By 2005, short sales and foreclosures were circling and damaging values of other houses, for example, the neighbors. A short sale is when the lender and buyer both agree that the loan cannot be paid and the home needs to go, although nobody wants a foreclosure because the bank does not want to lose money from the loan. Therefore, the loss is split in two with an attempt to sell the home, although, at a sacrificed, lower cost. A foreclosure, very simply, is when the bank owns your home because the original homeowner can no longer afford the loan on the mortgage. And rather than short sales and foreclosures, some people just abandoned their houses. |

|

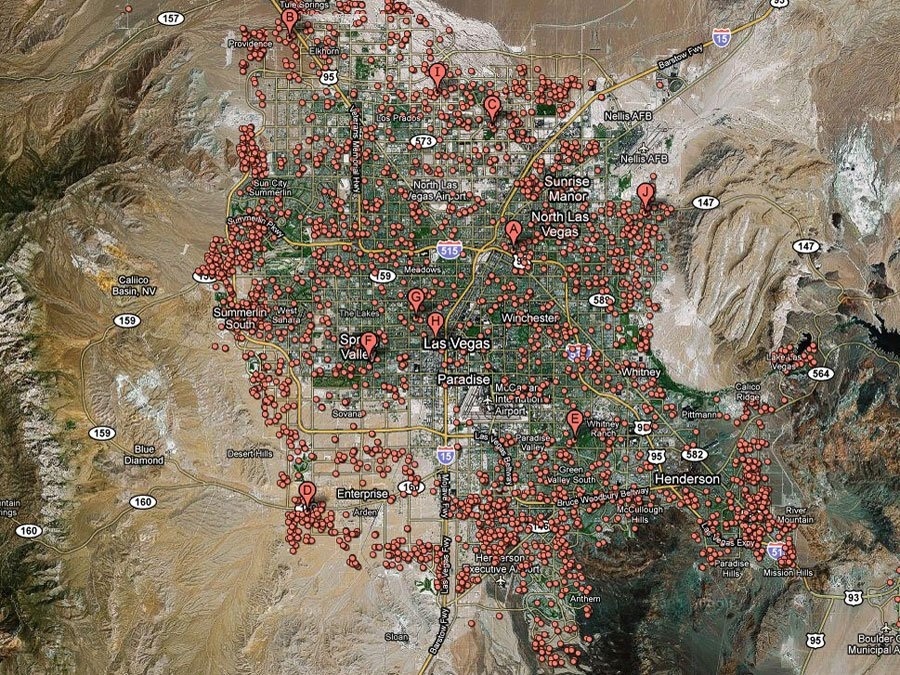

In this Las Vegas, during the crisis, every one in nine houses were forecloesed. Each dot represents a group of houses in the Las Vegas area.

|

In 2006, the banking problems began to present themselves, resulting in the first wave of layoffs. Immigration problems followed, when the government made plans to deport all illegal immigrants and, at this time, many latino families had been victim of predatory lending, which was explained earlier, because this strategy usually targeted a demographic like the elderly or the uneducated, those who, perhaps, wouldn’t understand the the corruption beneath the contract. They were trying to balance many jobs in order to pay the mortgages, but during deportation they would be fired, their incomes lost, and their houses foreclosed. And by 2007, the bubble finally burst with the subprime loans and predatory lending resulting in too many short sales and foreclosures, which caused major losses for banks and investors and, therefore, many layoffs.

Many American homeowners, about one-third, were “underwater”, meaning that their mortgage debt exceeded the the value of the house, a value that has constantly been lowered thanks to many houses left on the market as a result of foreclosures. These foreclosures and short-sales have leveled to more than $6 trillion concerning household wealth. Banks have reduced their tolerance and confidence in lending, and financial institutions have been affected as mortgage-backed securities continue to decline in value. |